Quick Answer: What Are the Basics of Personal Finance?

Personal finance basics refer to the foundational principles of managing your money effectively: building an emergency fund, budgeting your income, eliminating high-interest debt, saving consistently, and investing for long-term growth. Mastering these fundamentals in the right order creates a stable financial foundation that supports every other financial goal you will ever pursue.

Introduction

- Quick Answer: What Are the Basics of Personal Finance?

- Introduction

- Why Personal Finance Matters More Than Ever in 2026

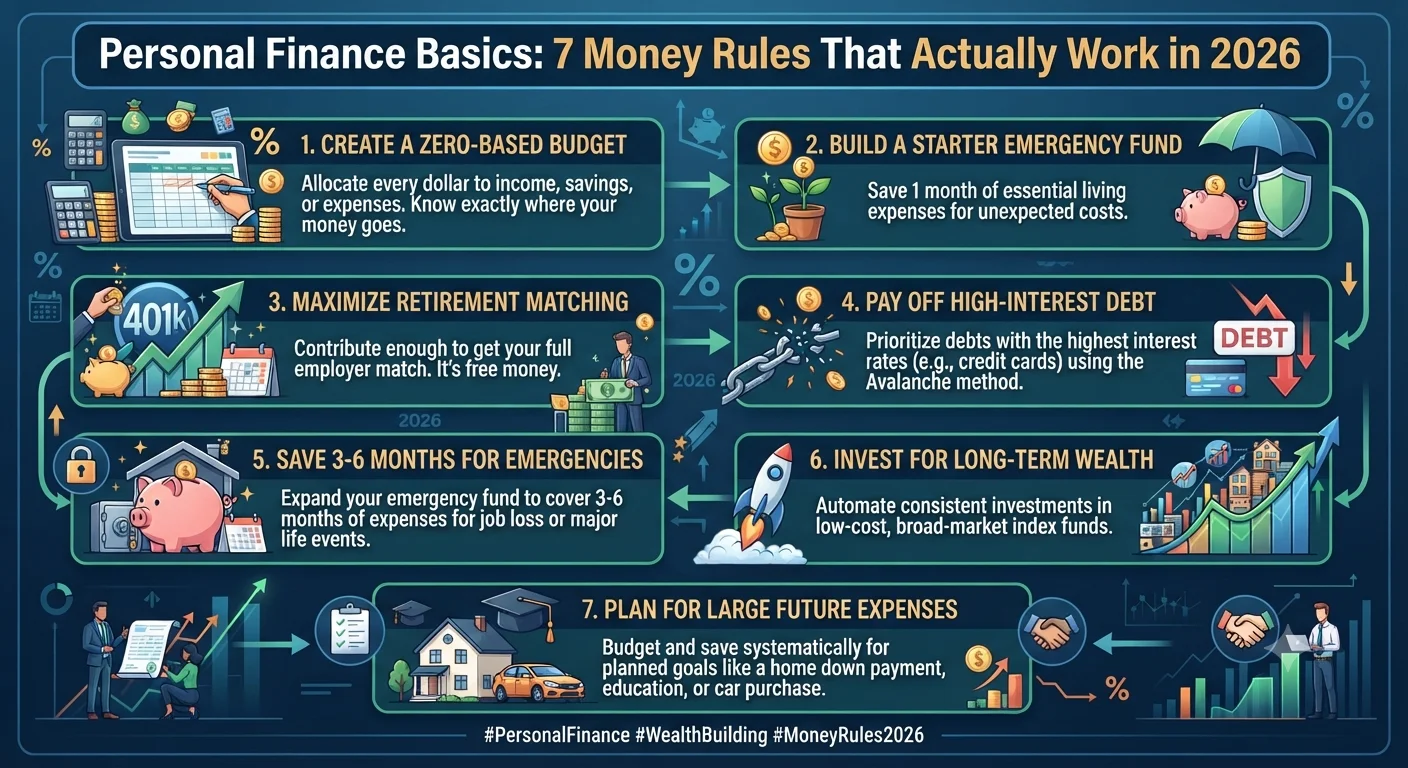

- Rule 1: Build an Emergency Fund Before Anything Else

- Rule 2: Follow the 50/30/20 Budget Framework

- Rule 3: Eliminate High-Interest Debt Aggressively

- Rule 4: Invest Early and Let Compound Interest Work for You

- Rule 5: Maximize Tax-Advantaged Accounts First

- Rule 6: Build Multiple Income Streams

- Rule 7: Protect Your Wealth With Insurance

- Key Takeaways

- Frequently Asked Questions

Most people spend more time planning a two-week vacation than they spend planning their entire financial future. This is not because people are careless. It is because personal finance is rarely taught in schools, rarely discussed openly in families, and often made to seem more complicated than it actually is by an industry that profits from complexity.

The truth is that the core principles of personal finance are not difficult to understand. They are difficult to execute consistently, because they require discipline, delayed gratification, and the willingness to make choices today that pay off years from now.

According to a 2024 survey by the Federal Reserve Bank of New York, approximately 37 percent of American adults would struggle to cover an unexpected expense of $400 without borrowing money or selling something. A 2023 Bankrate study found that 57 percent of US adults are uncomfortable with their level of emergency savings. These statistics are not unique to the United States. The International Monetary Fund has documented similar patterns of financial fragility across developed and developing economies alike.

The seven money rules in this guide are not theoretical. They are drawn from the consistent findings of behavioral economists, certified financial planners, and decades of research into what separates households that build lasting wealth from those that remain financially vulnerable. Apply them in order, and you will be further ahead financially within 12 months than most people manage in a decade.

Why Personal Finance Matters More Than Ever in 2026

The financial environment in 2026 presents both new opportunities and new challenges for individuals trying to manage their money wisely.

Interest rates, while having come down from the peaks of 2023, remain elevated by historical standards, meaning that carrying high-interest debt is more expensive than it has been in decades, and that savers who park money in high-yield savings accounts and money market funds can earn meaningful returns for the first time since the 2010s.

Inflation, while significantly reduced from its 2022 highs, has permanently raised the cost of living in most countries. The compounding effect of several years of elevated prices means that budgets that felt adequate in 2020 are now stretched thin. Understanding how to budget for this new cost reality is essential.

At the same time, technological tools available to individual savers and investors have never been more powerful. Automated investing apps, commission-free brokerage accounts, high-yield savings products, and comprehensive budgeting software have placed the capabilities once available only to wealthy clients in the hands of anyone with a smartphone.

The gap between those who understand and apply personal finance fundamentals and those who do not continues to widen. The seven rules that follow are designed to place you firmly on the right side of that gap.

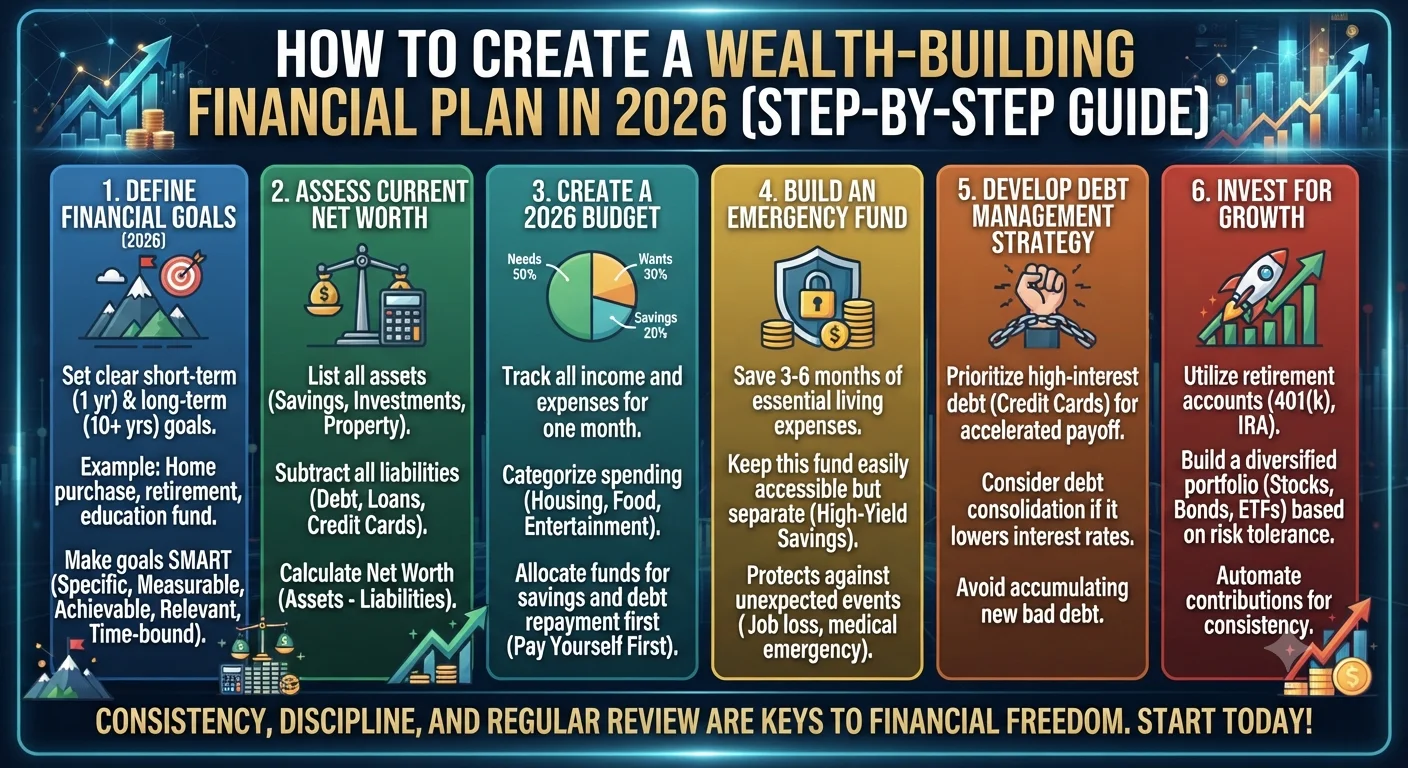

Rule 1: Build an Emergency Fund Before Anything Else

An emergency fund is a dedicated reserve of liquid cash set aside exclusively for genuine financial emergencies: unexpected medical expenses, sudden job loss, urgent car repairs, or essential home maintenance. It is not a travel fund. It is not a buffer for overspending. It is financial insurance against the unpredictable events that life reliably delivers.

The standard recommendation from most certified financial planners is to maintain an emergency fund covering three to six months of essential living expenses. Essential expenses include housing, utilities, food, transportation, and minimum debt payments. They do not include dining out, subscriptions, entertainment, or other discretionary spending.

For a household with $3,000 in monthly essential expenses, this means maintaining a fund of $9,000 to $18,000 in a liquid, easily accessible account. A high-yield savings account is the ideal vehicle, as it keeps the money separate from your regular checking account (reducing the temptation to spend it casually) while earning a meaningful interest rate that partially offsets inflation.

Why does this rule come first, before investing?

Without an emergency fund, any unexpected expense will force you to choose between taking on high-interest debt or liquidating investments, potentially at a loss during a market downturn. Research from the Urban Institute has shown that households with even modest emergency savings are significantly better positioned to avoid financial hardship during income disruptions than those without any buffer, regardless of income level.

Building your emergency fund is the financial foundation without which everything else is unstable. Once it is in place, you will find that you make better financial decisions across the board because you are no longer operating from a position of financial fragility.

How to build it faster:

Start by automating a transfer from your checking account to your high-yield savings account on the same day your paycheck arrives. Treat the emergency fund contribution like a non-negotiable expense. Even $100 or $200 per month adds up to $1,200 to $2,400 in a year, which for many people represents a significant portion of their target fund.

Rule 2: Follow the 50/30/20 Budget Framework

Budgeting is the foundation of all financial progress, yet most people either never create a budget or abandon theirs within weeks because it feels too restrictive or too complicated. The 50/30/20 framework, popularized by Senator Elizabeth Warren and Amelia Warren Tyagi in their book "All Your Worth," offers a simple, flexible structure that works for a wide range of incomes and lifestyles.

The framework divides your after-tax income into three categories:

50 percent for Needs. This category covers all essential, non-negotiable expenses: rent or mortgage, utilities, groceries, basic transportation, minimum loan payments, and necessary insurance premiums. If your needs currently consume more than 50 percent of your income, you face a structural budget problem that must be addressed by either reducing fixed costs (such as finding less expensive housing) or increasing income.

30 percent for Wants. This category covers lifestyle spending that improves quality of life but is not strictly necessary: dining out, streaming subscriptions, hobbies, clothing beyond basics, travel, and entertainment. Allowing 30 percent for wants prevents the budget from feeling punitive, which is one of the main reasons people abandon budgeting attempts. The key is remaining conscious of this spending rather than letting it drift unchecked.

20 percent for Financial Goals. This is the most important category for building wealth. It covers savings, emergency fund contributions, investment account contributions, and extra debt payments beyond the minimums. This 20 percent is the engine of your financial progress.

A practical implementation step is to open separate bank accounts for each category, funding them automatically from your primary account on payday. This physical separation makes it much easier to track spending and prevents money allocated for one category from being consumed by another.

For people with irregular income, such as freelancers or commission-based earners, the percentages remain the same but the calculation is based on your average monthly income over the previous three to six months, with adjustments made in particularly strong or weak months.

Rule 3: Eliminate High-Interest Debt Aggressively

High-interest debt is the single greatest obstacle to wealth building for most households. Credit card debt carrying an annual percentage rate of 20 to 29 percent (which is typical in the United States market as of 2026, according to Federal Reserve consumer credit data) is essentially impossible to outperform through investing. The stock market's long-term historical return of approximately 10 percent per year before inflation is less than half the interest rate many credit cards charge.

Every dollar of high-interest debt you carry is costing you more than you can realistically earn investing that dollar elsewhere. Eliminating it is therefore the equivalent of earning a guaranteed return equal to the interest rate you are paying, risk-free.

Two proven methods for debt elimination:

The Avalanche Method directs extra payments toward the debt with the highest interest rate first, while making minimum payments on all others. Once the highest-rate debt is paid off, you redirect those payments to the next highest-rate debt, and so on. This method minimizes the total interest paid over time and is mathematically optimal.

The Snowball Method, developed and popularized by personal finance educator Dave Ramsey, directs extra payments toward the smallest balance first regardless of interest rate. As each small debt is eliminated, the monthly payment amount that was servicing it is added to the attack on the next-smallest balance. This method produces quicker visible wins that many people find psychologically motivating, helping them maintain momentum over what can be a multi-year debt elimination process.

Research from the Kellogg School of Management at Northwestern University found evidence supporting the psychological effectiveness of the snowball method for many consumers, even though the avalanche method is mathematically superior. The best method is ultimately the one you will actually stick to.

Once high-interest consumer debt is eliminated, your monthly cash flow increases dramatically, freeing capital for savings and investment.

Rule 4: Invest Early and Let Compound Interest Work for You

Compound interest is the process by which the returns on an investment themselves generate further returns over time. It is often called the most powerful force in personal finance, and the data behind it justifies that description.

Consider two investors. Investor A begins investing $300 per month at age 25 and continues until retirement at 65, a total of 40 years and $144,000 in contributions. Investor B waits until age 35 to start investing the same $300 per month, investing for 30 years until age 65, contributing a total of $108,000. Assuming both earn an average annual return of 8 percent, Investor A retires with approximately $933,000. Investor B retires with approximately $408,000. The difference of $525,000 in retirement wealth was produced not by a greater investment amount but purely by starting 10 years earlier.

This example illustrates the fundamental rule: time in the market is more valuable than the amount invested.

Recommended Articles

PERSONAL FINANCE BUDGETING

PERSONAL FINANCE BUDGETING

For beginners, the most straightforward way to start investing is through an employer-sponsored retirement plan if one is available. If your employer offers a 401(k) match, contribute at least enough to capture the full match before directing funds anywhere else. An employer match is a guaranteed 50 to 100 percent immediate return on that portion of your contribution, which no other investment can reliably match.

Beyond employer accounts, low-cost index funds purchased through a tax-advantaged individual retirement account represent the most accessible and historically reliable path to long-term wealth accumulation for most individuals.

Rule 5: Maximize Tax-Advantaged Accounts First

The difference between investing inside a tax-advantaged account and investing in a standard taxable brokerage account is substantial over long time periods, yet many people never take full advantage of the accounts available to them.

In the United States, the primary tax-advantaged investment accounts are:

401(k) and 403(b) Plans (employer-sponsored retirement accounts): Contributions reduce your taxable income in the year they are made, and all investment growth is tax-deferred until withdrawal in retirement. As of 2026, individuals under 50 can contribute up to $23,500 annually to these accounts.

Individual Retirement Accounts (IRAs): Traditional IRAs provide the same tax-deferred growth as a 401(k), while Roth IRAs allow you to contribute after-tax dollars and withdraw both contributions and earnings completely tax-free in retirement. For long-term investors who expect to be in a higher tax bracket in retirement, Roth accounts are often particularly valuable. The annual contribution limit for IRAs in 2026 is $7,000 for individuals under 50.

Health Savings Accounts (HSAs): Available to those enrolled in high-deductible health plans, HSAs offer a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. After age 65, HSA funds can be withdrawn for any purpose (subject to ordinary income tax, similar to a traditional IRA), making them one of the most flexible tax-advantaged accounts available.

ISAs in the United Kingdom function similarly, allowing tax-free savings and investment growth up to an annual contribution limit.

Maximizing contributions to these accounts before investing in taxable accounts can add hundreds of thousands of dollars to your retirement wealth over a career through the compounding of tax savings alone.

Rule 6: Build Multiple Income Streams

The wealthiest households in every economy share a common characteristic: they do not rely on a single source of income. IRS data analyzed by financial researchers consistently shows that the majority of millionaires maintain three or more active income streams.

This is not simply about earning more money, though additional income obviously accelerates every financial goal. Multiple income streams provide financial resilience. If one stream is disrupted by job loss, illness, or economic disruption, the others continue to provide cash flow that prevents financial crisis.

Income streams broadly fall into three categories:

Active income requires your direct time and effort: your primary employment or professional practice, freelance work, consulting, or a part-time job. This is where most people start and often where the largest single income comes from.

Portfolio income comes from investments: dividends from stocks, interest from bonds, and capital gains from selling appreciated assets. This income grows over time as your invested assets accumulate, eventually reaching a scale where it can meaningfully supplement or even replace active income.

Passive income requires upfront effort or investment to establish but then generates ongoing income with minimal active management: rental property income, royalties from intellectual property, revenue from a digital product or online business, or income from a limited partnership.

Building additional income streams does not require becoming an entrepreneur or managing complicated businesses. Many people start simply by developing a marketable freelance skill related to their existing profession, which requires no startup capital and can be built gradually around existing employment commitments.

Rule 7: Protect Your Wealth With Insurance

All the financial progress you build can be erased by a single catastrophic event if you are not adequately protected. Insurance is the mechanism by which you transfer the financial risk of low-probability, high-consequence events to a third party in exchange for a predictable premium payment.

The essential types of insurance for most individuals and families are:

Health Insurance is the most critical protection for most people. Medical expenses are the leading cause of personal bankruptcy in the United States according to research published in the American Journal of Public Health. Even in countries with public health systems, private health coverage often provides faster access and broader coverage for significant medical events.

Life Insurance is essential for anyone who has financial dependents: a spouse, children, or other family members who rely on your income. Term life insurance, which provides a death benefit for a specified period (typically 20 to 30 years) at the most affordable premiums, is the appropriate product for most working-age adults with dependents. Whole life and universal life policies are significantly more expensive and often unnecessary for people who are diligently building investment portfolios.

Disability Insurance is the most commonly overlooked essential coverage. According to the Social Security Administration, one in four workers will experience a disability lasting three months or longer before retirement. Your ability to earn an income is your greatest financial asset, particularly early in your career. Disability insurance replaces a portion of your income if illness or injury prevents you from working.

Property Insurance protects your home and possessions. For homeowners, this is typically required by mortgage lenders. Renters frequently overlook renters insurance despite its low cost, leaving them exposed to potentially significant losses from theft, fire, or water damage.

Reviewing your insurance coverage annually and whenever you experience a major life change (marriage, children, home purchase, significant income increase) ensures that your protection remains appropriate for your current circumstances.

Key Takeaways

- Build an emergency fund of three to six months of essential expenses before investing, so that unexpected events cannot derail your financial plan or force you to liquidate investments at a loss.

- The 50/30/20 budget framework provides a simple, flexible structure: 50 percent for needs, 30 percent for wants, and 20 percent for financial goals.

- High-interest consumer debt costs more than you can reliably earn investing, making its elimination a guaranteed, risk-free financial priority.

- Starting to invest a decade earlier produces dramatically larger retirement wealth than investing a larger amount later, purely through the power of compounding.

- Tax-advantaged accounts like 401(k), IRA, and ISA amplify investment returns significantly by eliminating or deferring taxes on investment growth.

- Multiple income streams provide both acceleration of financial goals and resilience against income disruptions.

- Adequate insurance coverage protects accumulated wealth against catastrophic events that can otherwise undo years of financial progress.

Frequently Asked Questions

What is the most important personal finance rule? If forced to choose one, most certified financial planners point to building the emergency fund as the foundational first step. Without financial resilience against unexpected events, every other financial plan is vulnerable. The emergency fund is what separates people who can absorb life's inevitable surprises from those who are pushed into debt by them.

How much should I save per month? The standard recommendation is to save and invest at least 20 percent of your after-tax income. This target comes from the 50/30/20 budget framework and is supported by research on the savings rates needed to achieve financial independence within a reasonable working career. If 20 percent is not immediately achievable, start with whatever is possible and increase the percentage by one to two percentage points with each income increase until you reach the target.

Is personal finance the same in every country? The core principles of personal finance apply universally: spend less than you earn, eliminate debt, save consistently, invest for long-term growth, and protect what you build. The specific products, tax treatment, and regulatory environment vary significantly by country. The general principles in this guide apply broadly, but specific account types, contribution limits, and tax rules should be verified for your country of residence.

What should I do first: pay off debt or invest? The answer depends on the interest rate of your debt. For debt carrying interest rates above approximately 6 to 7 percent annually, paying it down aggressively typically produces a better risk-adjusted return than investing in the market. For low-interest debt such as a typical mortgage or student loan, maintaining minimum payments while investing the remainder can be mathematically sensible over long periods. Always prioritize capturing any employer retirement account match before accelerating debt repayment, as the match represents an immediate guaranteed return.

How long does it take to see results from good personal finance habits? Financial progress often feels slow in the early stages but accelerates dramatically over time as compounding takes hold. Within the first year of disciplined budgeting and saving, most people see meaningful debt reduction and emergency fund growth. Within three to five years, consistent investors who contribute regularly to market-linked accounts typically see their portfolio begin growing faster through investment returns than through their own contributions. The compounding of positive habits, like the compounding of money itself, produces exponentially growing results over a 10 to 20 year horizon.

Do I need a financial advisor to implement these rules? For the foundational rules in this guide, a financial advisor is not strictly necessary. Building an emergency fund, budgeting, eliminating debt, and contributing to index funds through a low-cost brokerage account are all actions that can be taken independently with freely available educational resources. Where a financial advisor adds significant value is in more complex situations: estate planning, tax optimization with multiple income streams, business ownership, significant wealth management, or navigating complex benefit elections. Look for a fee-only fiduciary advisor, who is legally required to act in your best interest rather than earning commissions from product recommendations.

RISK DISCLAIMER: This article discusses personal finance concepts for educational purposes only. It does not constitute personalized financial, tax, or legal advice. Tax laws, contribution limits, and financial regulations vary by country and change over time. Please consult with qualified professionals in your country of residence before implementing financial strategies.