Quick Answer: How Do You Create a Financial Plan?

Creating a financial plan involves eight sequential steps: calculating your current net worth, defining specific financial goals, building a monthly budget, establishing an emergency fund, eliminating high-interest debt, starting a systematic investment program, building multiple income streams, and protecting your wealth with appropriate insurance. Each step builds on the previous one, creating a compounding foundation of financial security that grows stronger every year it is maintained.

Introduction

- Quick Answer: How Do You Create a Financial Plan?

- Introduction

- Why 78% of People Live Paycheck to Paycheck Without a Plan

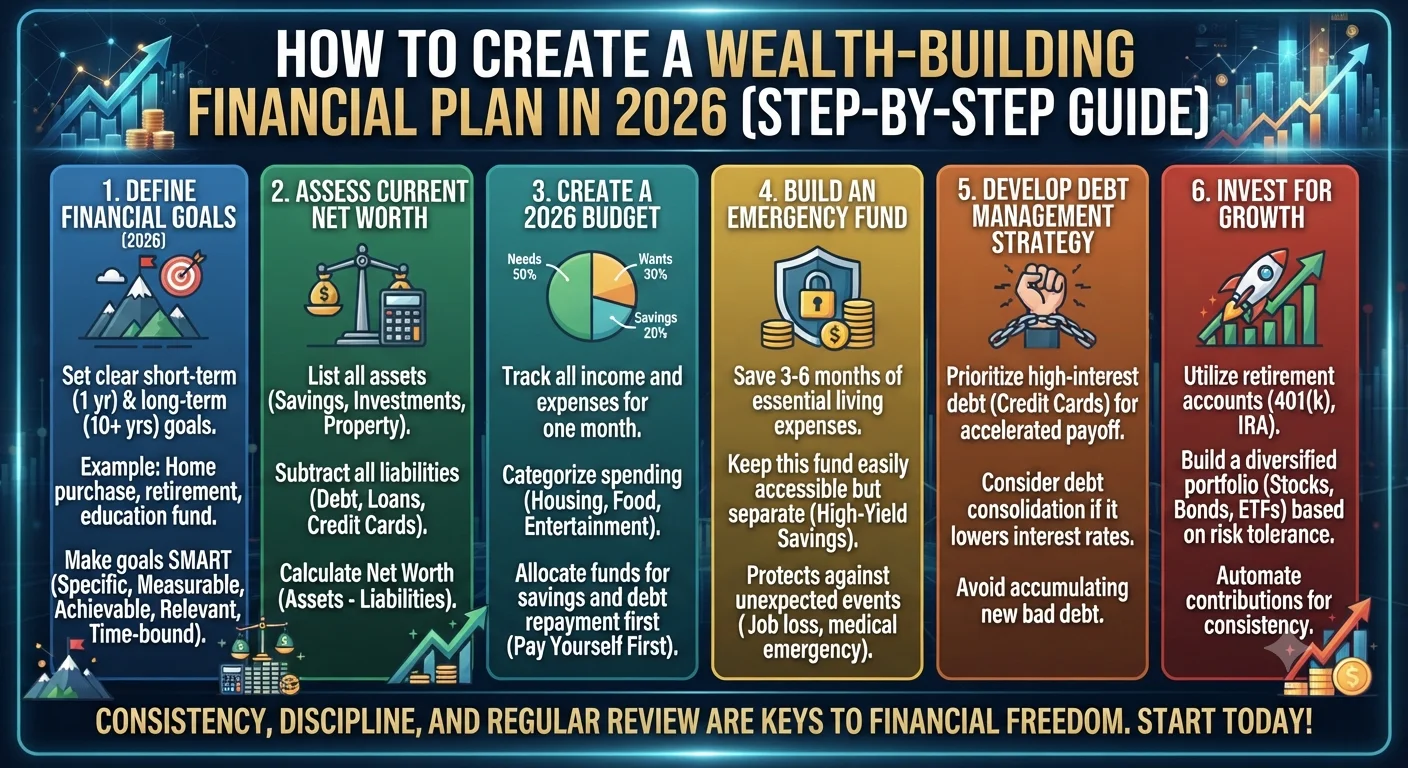

- Step 1: Calculate Your Net Worth and Current Financial Position

- Step 2: Define SMART Financial Goals for 2026 to 2031

- Step 3: Create a Monthly Budget Using the Zero-Based Method

- Step 4: Build Your Emergency Fund Before Investing

- Step 5: Eliminate Consumer Debt Using the Avalanche Method

- Step 6: Start Investing With Correct Asset Allocation by Age and Risk Profile

- Step 7: Build Multiple Income Streams

- Step 8: Protect Your Plan With Insurance

- Key Takeaways

- Frequently Asked Questions

Most people manage their finances reactively. Money comes in, money goes out, and whatever remains at the end of the month is saved or spent on impulse. When asked about their financial plan, the honest answer for the majority of households is that they do not have one. They have financial habits, some good and some destructive, and they have vague aspirations about retirement and security that have never been translated into specific, actionable targets.

The consequences of this reactive approach compound over time just as powerfully as interest compounds in a savings account, but in the opposite direction. Without a plan, financial decisions are made in isolation, without reference to long-term goals. The car lease that costs $400 per month is evaluated as a monthly affordability question, not as a $28,800 five-year commitment that could instead be invested and grow to $42,000 at a 7 percent return. The credit card balance that "will be paid off soon" remains for years, costing thousands in interest while the opportunity to invest those interest payments passes permanently.

A financial plan transforms this reactive pattern into a proactive one. It does not require a financial advisor, complex software, or a high income to create. It requires honesty about your current situation, clarity about your goals, and the discipline to follow a structured process to closing the gap between where you are and where you want to be.

The eight-step process in this guide is applicable to individuals and families at any income level. The specific numbers will differ, but the structure is universal.

Why 78% of People Live Paycheck to Paycheck Without a Plan

Before the steps, the context. A 2024 survey by LendingClub found that approximately 65 percent of Americans were living paycheck to paycheck, including a significant proportion of individuals earning above-average incomes. This counterintuitive finding, that income alone does not determine financial security, points directly to the role of financial planning.

Research consistently shows that lifestyle inflation, spending that automatically rises with income rather than remaining disciplined so that savings increase, is the primary mechanism by which high earners fail to build wealth. The person earning $200,000 per year who spends $195,000 is in a structurally similar financial position to the person earning $50,000 who spends $48,000. Both are building wealth at the same rate. Both are one significant financial disruption away from crisis.

A financial plan addresses this by making explicit decisions about the relationship between income and spending rather than allowing that relationship to be determined by default and circumstance.

Step 1: Calculate Your Net Worth and Current Financial Position

The foundation of any financial plan is an accurate, honest assessment of where you currently stand. Net worth is the single most comprehensive measure of financial health. It is calculated as total assets minus total liabilities.

Your assets include:

All cash and savings accounts (current balances), investment accounts including brokerage accounts, retirement accounts (401k, IRA, pension), and education savings accounts, the current market value of any real estate you own, the current market value of vehicles you own, and any other valuable property or business interests.

Your liabilities include:

All outstanding debt balances: mortgage balance, car loan balance, student loan balances, credit card balances, personal loan balances, and any other obligations you are legally required to repay.

Subtracting total liabilities from total assets produces your net worth. A positive net worth means your assets exceed your obligations. A negative net worth means your debts exceed your assets, which is common for young adults with significant student loan debt and is not a crisis in itself, but it establishes a clear starting point.

Beyond the net worth snapshot, document your monthly cash flow: total monthly after-tax income from all sources minus total monthly expenses across all categories. This cash flow figure is the raw material from which financial progress is made. A positive cash flow means you have money available to direct toward financial goals. A negative cash flow means you are currently living beyond your means and must address this before any other financial planning can succeed.

Step 2: Define SMART Financial Goals for 2026 to 2031

A goal without a deadline and a specific target is a wish. SMART goals are Specific, Measurable, Achievable, Relevant, and Time-bound. They transform aspirations into targets that can be planned for, tracked, and achieved.

Examples of converting vague aspirations into SMART financial goals:

Vague: "I want to save more money." SMART: "I will save $12,000 by December 31, 2027 by automatically transferring $500 per month from my checking account to my high-yield savings account beginning in August 2026."

Vague: "I want to pay off my credit cards." SMART: "I will eliminate my $8,400 credit card balance across two cards by directing $700 per month to debt repayment using the avalanche method, achieving zero credit card debt by August 2027."

Vague: "I want to invest for retirement." SMART: "I will contribute $6,000 to my Roth IRA in 2026 and 2027, increasing to the maximum allowable contribution as income grows, targeting an investment portfolio of $500,000 by age 55."

Categorize your goals by time horizon: short-term goals have timelines of one to three years (emergency fund, vacation, debt payoff), medium-term goals span three to ten years (down payment on property, starting a business, children's education), and long-term goals extend beyond ten years (retirement, financial independence).

Quantifying each goal in dollar terms and assigning a specific completion date allows you to calculate exactly how much you need to save or invest each month to reach it. This calculation anchors your budget to your goals rather than leaving both as separate, unconnected activities.

Step 3: Create a Monthly Budget Using the Zero-Based Method

With your current financial position documented and your goals quantified, the budget is the operational mechanism that directs your income toward those goals each month. The zero-based budgeting method assigns every dollar of income a specific purpose before the month begins, leaving zero unassigned and unaccounted for.

The process begins by listing your total monthly after-tax income from all sources at the top of your budget. Then allocate this income across all expense categories until the total expenses plus savings and investment contributions equal the total income exactly.

Fixed expenses are consistent and mandatory each month: rent or mortgage, car payment, insurance premiums, minimum debt payments, and subscription services. These are entered at their exact amounts.

Variable necessary expenses are required but fluctuate: groceries, utilities, transportation fuel, and medical copays. Budget these based on a three-month average of actual spending, which you can find by reviewing bank and credit card statements.

Savings and investment contributions are treated as non-negotiable expenses, allocated before discretionary spending rather than from whatever remains after other spending. This "pay yourself first" structure is the defining characteristic of budgets that actually build wealth.

Discretionary expenses fill the remainder: dining out, entertainment, clothing, hobbies, and gifts. These are the adjustable levers that can be reduced when the budget needs to accommodate additional savings or debt repayment.

If your income minus non-negotiable fixed expenses, necessary variable expenses, and savings contributions leaves insufficient funds for discretionary spending and the budget does not balance, you have two paths: reduce discretionary spending or increase income. The budget forces this trade-off to become explicit rather than being resolved unconsciously by simply running out of money before the month ends.

Step 4: Build Your Emergency Fund Before Investing

As covered in the personal finance basics article, the emergency fund is the prerequisite for all other financial planning. Until you have three to six months of essential expenses in a liquid, separate savings account, aggressive debt repayment and investing must be balanced against maintaining at least a small cash buffer.

A practical staging approach for those starting from zero: build a starter emergency fund of $1,000 to $2,000 as quickly as possible before aggressively attacking debt. This buffer prevents a small unexpected expense from derailing your debt repayment progress by forcing you to add to credit card balances. Once high-interest debt is eliminated, build the emergency fund to its full three-to-six-month target before maximizing investment contributions.

The emergency fund should be held in a high-yield savings account separate from your everyday checking account, close enough to access within one to three business days if genuinely needed but not so immediately accessible that it is drawn down for non-emergencies.

Step 5: Eliminate Consumer Debt Using the Avalanche Method

High-interest consumer debt is the most reliable wealth destroyer in most household budgets. Every month that a credit card balance carrying 20 percent annual interest remains unpaid, that interest compounds against you at a rate no conservative investment can match in reverse.

Recommended Articles

PERSONAL FINANCE BUDGETING

PERSONAL FINANCE BUDGETING

The debt avalanche method, which is mathematically optimal, works as follows. List all your debts in order from the highest interest rate to the lowest. Make the minimum required payment on every debt each month. Direct all additional available dollars toward the highest-interest debt until it is completely eliminated. Then redirect the payment you were making on the paid-off debt (plus the minimum that was already being made on the next debt) toward the second-highest-rate debt. Continue this sequence until all consumer debt is eliminated.

Document this plan in your budget. Calculate the exact month in which each debt will be paid off at your current payment rate using a debt payoff calculator (freely available through many personal finance websites). This visualization of the payoff timeline converts an abstract obligation into a concrete countdown that maintains motivation through what is often a multi-year process.

Step 6: Start Investing With Correct Asset Allocation by Age and Risk Profile

With high-interest debt eliminated and an emergency fund in place, the investing phase begins. The first priority is maximizing contributions to tax-advantaged retirement accounts before investing in taxable brokerage accounts, because the tax-free or tax-deferred growth inside these accounts compounds significantly faster than equivalent returns in taxable accounts.

Asset allocation is the division of your investment portfolio across different asset classes: stocks (equities), bonds (fixed income), cash equivalents, and alternative investments. The appropriate allocation for any individual depends on their time horizon and risk tolerance.

A widely used starting framework is the rule of 110 minus age. Subtract your age from 110, and the result suggests the approximate percentage of your portfolio to hold in stocks, with the remainder in bonds and cash. At age 30, this suggests approximately 80 percent stocks and 20 percent bonds. At age 50, it suggests 60 percent stocks and 40 percent bonds. This framework reflects the principle that younger investors can accept more volatility because they have more time to recover from downturns, while those approaching retirement should shift toward capital preservation.

For most individual investors, particularly those starting out, implementing this allocation through a handful of low-cost index funds is the most efficient approach:

A total US stock market index fund provides broad exposure to the entire US equity market in a single fund. An international equity index fund adds geographic diversification outside the US. A US bond market index fund provides the fixed income component. A combination of these three funds, in proportions matching your target allocation, is the complete portfolio structure used by many sophisticated investors including Nobel laureate William Sharpe, who has advocated for simplicity and low costs as the core of effective investing.

Step 7: Build Multiple Income Streams

Once your investment program is established and running automatically, the most impactful next lever for accelerating financial progress is increasing income. Passive income development (covered in the passive income ideas article) is the long-term goal, but active income growth is the fastest path to improving monthly cash flow in the shorter term.

Identify the skills and expertise you have developed in your primary career that carry transferable market value. Freelance consulting, advisory work, coaching, speaking, or contract work in your area of professional expertise can generate meaningful supplemental income without requiring the investment of time needed to build a fully passive income stream.

Additionally, evaluate opportunities to increase your primary income through professional development, skill acquisition, performance-based advancement, or career transitions. Research by the Bureau of Labor Statistics consistently shows that voluntary job changes produce larger wage increases on average than staying in the same role with the same employer, a data point relevant to anyone who has not reviewed their market compensation in several years.

Every dollar of additional income, when directed toward your financial goals rather than absorbed by lifestyle inflation, dramatically accelerates the timeline to financial independence.

Step 8: Protect Your Plan With Insurance

The final step is protecting everything you have built. A single uninsured catastrophe, whether a major medical event, disability, liability lawsuit, or natural disaster, can eliminate years of financial progress. Insurance converts this catastrophic tail risk into a manageable, predictable premium.

Review the essential coverages: health insurance (catastrophic medical event protection), life insurance (income replacement for dependents if you die prematurely), disability insurance (income replacement if illness or injury prevents you from working, your most valuable financial asset is your income-generating capacity), liability umbrella insurance (protection above the limits of home and auto policies), and property insurance (home or renters insurance protecting physical assets).

Review coverage annually and after major life events. As your net worth grows, coverage needs change. The amount of life insurance appropriate for a 28-year-old with a spouse, two young children, a mortgage, and no other assets is very different from what is appropriate at 50 with adult children, a paid-off home, and a $1 million investment portfolio.

Key Takeaways

- A financial plan begins with an honest calculation of your current net worth and monthly cash flow, establishing a baseline from which all progress is measured.

- SMART goals (Specific, Measurable, Achievable, Relevant, Time-bound) convert vague financial aspirations into specific targets with calculable monthly funding requirements.

- Zero-based budgeting assigns every dollar of income a specific purpose before the month begins, treating savings and investment contributions as non-negotiable expenses allocated before discretionary spending.

- The correct sequencing of financial priorities is: emergency fund starter buffer, then aggressive high-interest debt elimination, then full emergency fund completion, then maximizing tax-advantaged investment accounts, then taxable investment accounts.

- Asset allocation appropriate to your age and risk profile, implemented through low-cost index funds, provides the investment framework that accumulates wealth over time with minimal ongoing management.

- Income growth, through career advancement, supplemental active income, and long-term passive income development, is the most powerful accelerator of financial progress once the budget and investment framework are in place.

- Insurance coverage protecting against catastrophic loss events is the final component that ensures your financial plan survives the inevitable unexpected disruptions of a human life.

Frequently Asked Questions

How long does it take to create a financial plan? A basic but functional financial plan covering steps one through four can be created in a focused weekend of honest work: pulling account statements, calculating net worth and monthly cash flow, defining three to five specific goals with timelines, and building a zero-based budget. The plan itself is simple to create. The value comes from following it consistently over months and years, and from reviewing and updating it at least annually to reflect changed circumstances and progress toward goals.

Do I need a financial advisor to create a financial plan? For the foundational steps of financial planning described in this guide, a financial advisor is not strictly necessary. The skills required are organizational and mathematical rather than specialized, and all the information needed is freely available. Where a fee-only fiduciary financial advisor adds significant value is in more complex situations: estate planning, tax optimization with multiple income sources, business succession planning, insurance analysis, and detailed retirement income projections. When selecting an advisor, always look for fee-only (paid directly by you, not through product commissions) and fiduciary (legally required to act in your best interest) credentials.

What is the biggest financial planning mistake most people make? The most universally damaging financial planning mistake is failing to start. The second most costly is starting late. The mathematics of compound growth reward early action so dramatically that the difference between starting to invest at 25 versus 35 produces a retirement wealth gap that is impossible to close through any amount of increased later contributions. The best time to start a financial plan is the moment you have your first regular income. The second-best time is right now.

How often should I review and update my financial plan? At minimum, a formal annual review of your financial plan is appropriate: recalculating your net worth, comparing your actual spending and saving rates to your budget, assessing progress toward each goal, and adjusting contributions or timelines based on what changed. Additionally, review your plan immediately after any major life change: marriage or divorce, birth of a child, job change, significant income change, inheritance, major debt addition (mortgage), or the death of a family member. Life changes frequently alter both your financial situation and your goals simultaneously.

Can I follow a financial plan if my income is irregular? Yes, though irregular income requires some adjustments to the standard framework. Rather than budgeting based on a fixed monthly income, calculate your minimum reliable monthly income (the amount you can virtually guarantee even in poor months) and build your fixed expenses and minimum savings targets around that figure. In above-average income months, allocate the surplus according to a predefined priority order: top up savings to the monthly target, make extra debt payments, increase investment contributions. This variable savings approach captures the upside of good months without overcommitting expenses that must be maintained during lean periods.

RISK DISCLAIMER: This article provides educational financial planning information and does not constitute personalized financial, tax, or legal advice. All investment and financial strategies carry risk. Results depend on individual circumstances, market conditions, and execution consistency. Please consult qualified professionals before implementing significant financial decisions.